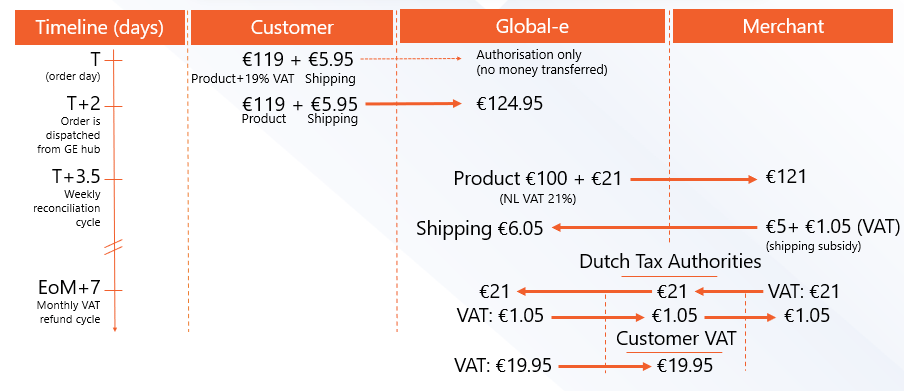

- Product price in Europe = €121 (€100 + 21% VAT) - exported into the EU (Germany)

- Shipping cost €10 , charged to customer €5 (shipping subsidy €5)

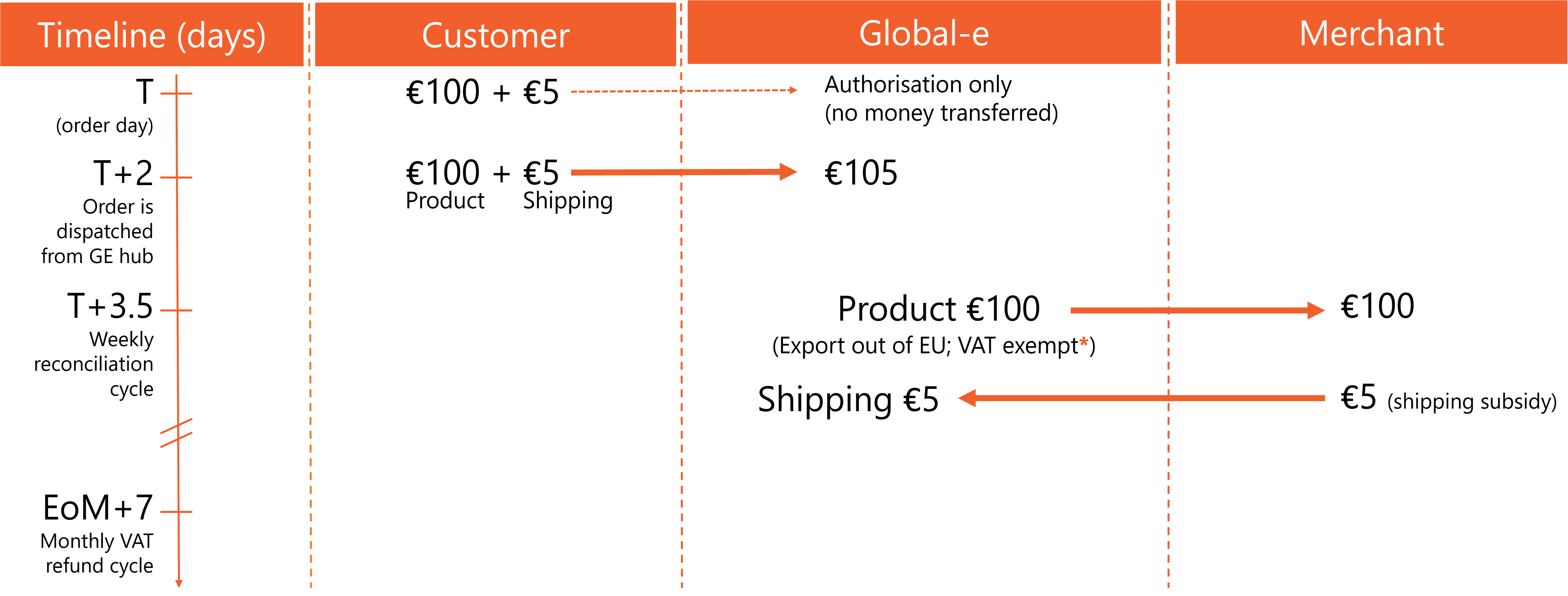

- Product price in Europe = €121 (€100 + 21% VAT) - exported out of the EU

- Shipping cost €10 , charged to customer €5 (shipping subsidy €5)

While the sale is a domestic sale between two Dutch entities, since the final destination of the goods is outside of the EU, a VAT exemption applies.

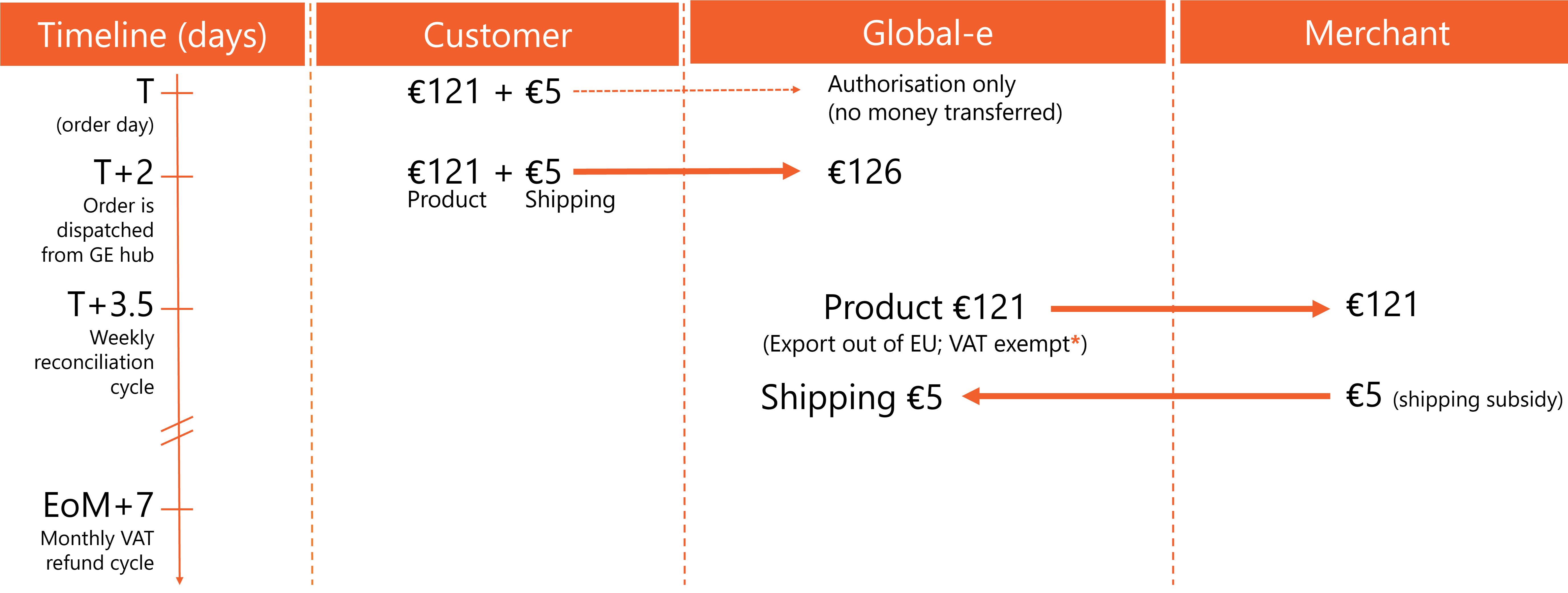

- Product price in Europe = €121 (€100 + 21% VAT) - exported out of the EU

- Shipping cost €10 , charged to customer €5 (shipping subsidy €5)

While the sale is a domestic sale between two Dutch entities, since the final destination of the goods is outside of the EU, a VAT exemption applies.